One of the most important aspects of maintaining good credit is knowing your credit score. You can check your score for free every four months or once a year. Most credit card companies also offer free FICO score reports. If possible, it is a good idea at least to review your credit score three times per year.

Hard inquiries can affect your credit score

While you may not realize it, hard inquiries can negatively impact your credit score. When a creditor inquires about your credit report, this is called a hard inquiry. These inquiries often occur due to identity theft or error. Routine credit monitoring can help to identify errors. You can send a dispute correspondence to the credit bureau if you find an error. You can also contact your lender to dispute the inquiry and report fraud to the Federal Trade Commission.

Hard inquiries can generally reduce your credit score by one to five percentage points. The exact amount will depend largely on your credit score as well as the length of time since you last inquired. If you are not absolutely required to, it is better to limit the number of inquiries.

Your credit score is determined by your ability to make timely payments

Making timely payments is one of the key factors that will determine your credit score. Late payments can make it more difficult to repay your debt. Another factor is how much credit you have available compared to your total debt. High credit balances are a problem for lenders. Keep your credit utilization to a minimum of 30 percent. It is possible to improve your credit score by avoiding credit cards, and paying off any existing credit cards.

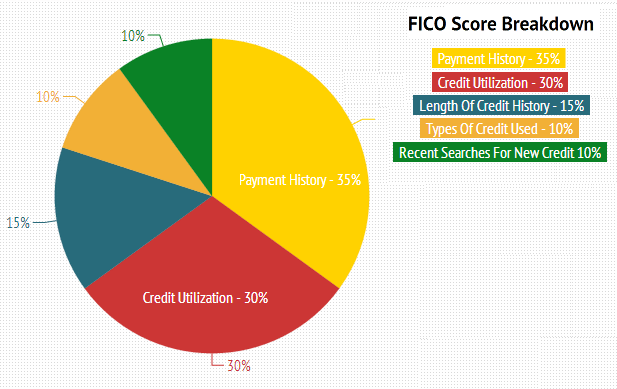

35% of your credit score is determined by your payment history. This information reveals if you have paid your bills on time and if you have missed payments. This information is used by lenders to assess your ability to repay your debts on a timely basis. Late payments are bad news because they hurt your score, but if you have a long payment history, your score will be much higher.

Dispute inaccurate information from your credit report

The credit bureaus can be contacted if they believe you have incorrect credit reports. They must investigate and provide a copy your credit report. The bureau might not agree with you, and the item will be added to your credit report. There are two options. You can either contact the creditor for clarification or re-dispute it with further information.

The best way to dispute inaccurate information is to write a dispute letter. Include a dispute template and copies of all supporting documents. Use the dispute address listed on the credit card report to send your dispute letter. It should be sent certified mail, along with a copy of the return receipt.

False information on your credit reports can adversely impact your credit score. It can also affect your ability of borrowing money or getting credit cards. Although the process is not complicated, it can be frustrating if you don't get your desired result. It's worthwhile if you get a complete report.